Vertex uses cookies to make our website work properly and to provide the most relevant content and services to our clients and site visitors. View our Privacy Policy.

Hidden Exterior Risks: Quantifying Concealed Liabilities in Real Estate Portfolios

July 9, 2026

Share

Property owners are operating in a complex new risk environment compared to just a few short years ago. According to Federal Reserve research, multifamily insurance costs increased sharply between 2019 and 2024, far outpacing inflation. At the same time, high-profile structural failures have prompted greater scrutiny of building safety, reserve funding, inspections, and deferred maintenance. As capital remains expensive, many owners are holding aging assets longer, delaying major expenditures, and treating physical building conditions as part of portfolio risk management.

The Invisible Liability

The problem is that many of the hidden exterior risks impacting asset value sit within the building envelope, beneath waterproofing systems, inside roof assemblies, and within exterior structures that may show few outward signs of deterioration. By the time water intrusion appears inside a unit, a tenant complaint surfaces, or a transaction uncovers missing records, the underlying condition may have been developing for years.

At Vertex, my team works with institutional investors, life insurance companies, private equity firms, lenders, developers, and real estate owners across hundreds of projects nationwide, ranging from $10 million developments to multi-billion-dollar assets. Through our building envelope consulting, risk evaluation, forensic investigation, and project advisory work, we see firsthand how exterior conditions can evolve long before they become emergencies and how quickly technical issues can escalate into a corporate business crisis.

What begins as a roof concern, balcony inspection, water intrusion complaint, or missing closeout record can quickly affect capital planning, insurance renewals, refinancing, transactions, claims, and long-term asset performance.

Shifting from a reactive maintenance approach to a proactive risk management strategy often helps owners better protect their assets. Let’s take a closer look at why exterior building conditions are receiving greater scrutiny, how deterioration can affect real estate portfolios, and what owners can do before they become an expensive surprise.

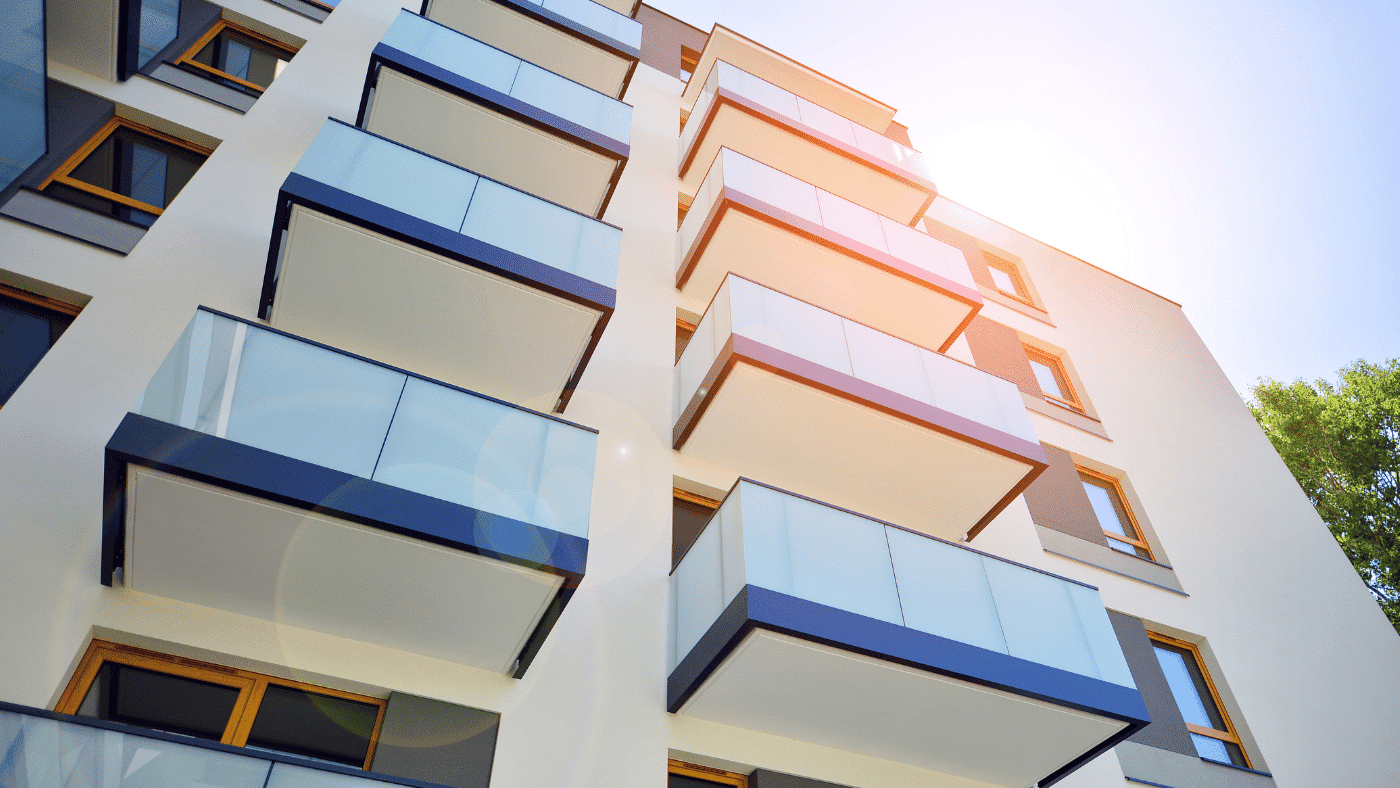

Balcony Compliance is Only the Starting Point

On June 16, 2015, a balcony collapsed in Berkeley, California, killing six people and severely injuring seven others. The failure was linked to water exposure and deterioration of the balcony’s wood framing. Subsequent forensic investigations found that significant water damage, fungal growth, and structural deterioration can remain hidden behind finished surfaces until invasive inspection reveals the underlying condition.

Vertex participated in the forensic investigation following the collapse and later contributed technical expertise as California developed new inspection requirements for exterior elevated elements. The resulting legislation, Senate Bills 721 and 326, established statewide inspection requirements for balconies, decks, walkways, stairways, and their associated waterproofing systems, fundamentally changing how owners evaluate concealed deterioration.

For apartment owners, condominium associations, and multifamily portfolio managers, the first response was operational. Which properties fall under the law? How many elements need to be reviewed? Under SB 721, inspectors must evaluate at least 15% of each type of exterior elevated element, including the load-bearing components and associated waterproofing systems.

For many owners, those inspections became the starting point for a broader discussion about portfolio risk. Property condition assessmentscan expand the conversation beyond a required repair to evaluate maintenance history, reserve assumptions, water management, documentation, and longer-term capital planning.

In our work, I’ve seen some owners use that process as a starting point rather than the end of the exercise. A required review may begin with one localized repair, but it can also expose broader patterns in water management, maintenance practices, reserve assumptions, repair history, or documentation.

After working with California’s balcony inspection framework, one client asked our team to apply a similar risk-mitigation approach across a 16-property portfolio nationwide. The work moved from a state-specific compliance lens to a broader review of exterior exposure across the portfolio nationwide.

A required balcony inspection provides an opportune moment for owners to voluntarily assess a much broader portfolio risk conversation.

When Exterior Problems Become Operational Risk

Insurance requirements, evolving regulations, inspections, and reserve planning are putting new pressure on owners to understand building conditions before localized exterior issues affect safety, operations, or asset value.

The 2021 Champlain Towers South collapse in Surfside, Florida, killed 98 people and led Florida lawmakers to pass new structural safety and reserve requirements for condominium buildings. Similar conversations have advanced in other states, including New Jersey and Maryland. Multifamily insurance costs have also continued to climb, making building condition, maintenance history, water intrusion, and deferred repairs harder to treat as routine property management issues.

Owners experience those pressures in several ways:

Expanding work order: A roof leak may begin with a simple repair, then expand once the assembly is opened and moisture damage is found beyond the visible leak.

Hidden deterioration: Exterior conditions may appear isolated while concealed deterioration may be present behind the exterior cladding, weather-resistive barrier (WRB), or concealed structural framing.

Transaction staller: Missing inspection records or repair history may give a buyer, lender, or insurer a reason to slow down or demand a discount.

Emergency conditions make those repair decisions harder. Once tenants are affected, access is restricted, or repair work has to be sequenced around an active property, the owner has less room to compare alternatives or estimate exposure. Work that could have been planned through capital budgeting or due diligence can become a compressed decision with more cost and less control. As exposure continues, the underlying condition may keep deteriorating.

Industry guidance is moving in the same direction. TheNational Institute of Building Sciencesdescribes building enclosure commissioning as “a process for validating whether enclosure materials, components, assemblies, systems, and design meet owner project requirements.” Visible damage is only part of the picture.

Owners also need to understand how the exterior systems are performing over time and where future risk may be developing. Some treat each exterior issue as a stand-alone repair. Others use building envelope due diligence to determine whether a roof concern, façade assessment, or water intrusion investigation points to a larger pattern across the portfolio.

Rather than seeking a cheap inspection. Looking for accurate, data-driven assessments that allow for informed capital and maintenance planning.

A pending acquisition, refinancing effort, insurance renewal, or planned disposition can put new attention on physical condition. A roof replacement that once sat comfortably in a future capital plan may move up once active leaks, warranty gaps, or related waterproofing issues are documented. A façade concern that looks limited from the ground may require a different conversation once access, concealed deterioration, tenant impact, or repair sequencing are understood.

Across large portfolios, the challenge is understanding which conditions deserve attention now, which can be planned for, and where the next hidden exterior risk is most likely to come from.

Why Your Records Are as Fragile as Your Roof

Many owners don’t discover documentation problems until someone else asks for the file.

A buyer wants to understand the repair history. A lender requests support for the condition of the asset. An insurer asks about prior maintenance. A claim requires records that show who did what, when, and why. At that point, the building may not be the only issue. The owner also has to prove the story behind the building.

At Vertex, we advocate for closeouts from the beginning of a project. The record should not be assembled months later from scattered emails, old folders, inconsistent file names, and memories of people who have already moved on.

A transaction-ready closeout file may include:

Warranties, operations, and maintenance manuals.

Inspection records and repair history.

Certificates of substantial completion.

Architect and engineer certifications.

Affidavits and contractor documentation.

Environmental or regulatory records.

Photos, drawings, reports, and supporting correspondence.

A well-organized file can be as valuable as a well-maintained asset during due diligence, refinancing, claims, or sale preparation.

I often use early site work as a hidden exterior risk example. If contaminated soil is removed during the first phase of a project, the regulatory paperwork needs to be collected when that scope is complete. Waiting until final closeout can leave the owner trying to rebuild a record long after the crews, consultants, and regulators involved in that work have changed.

The same principle applies to building envelope work. A roof repair, façade investigation, water intrusion investigation, or construction defect investigation should leave behind a clear record of what was observed, who evaluated it, what was repaired, which warranties apply, and which reports support the decision.

Thorough documentation can help mitigate the time, uncertainty, and assumptions that frequently surface when an asset changes hands or a building condition is challenged years later.

The Elements of a Technical Repair Plan

By the time an exterior issue reaches my team, the owner usually needs more than confirmation that something is wrong. They need to know what caused it, how far it goes, who needs to be involved, and what decisions have to be supported by the record.

Water intrusion is a good example. ASTM E2128 recognizes that leakage evaluations should look beyond the first visible stain or leak path and consider surrounding components, adjacent construction, service history, and performance expectations. For an owner, the visible damage is only the starting place.

The investigation should also clarify what kind of response the owner actually needs. Some conditions call for monitoring or maintenance. Others require repair planning, contractor coordination, claims support, or a deeper construction defect investigation. The point is to avoid treating every hidden exterior risk in the same way.

Unfortunately, issues can move into disputes. Ourstatistical analysis of building envelope failures from 2011 to 2019 shows why the record matters. Once owners, attorneys, insurers, contractors, and other stakeholders become involved, the conversation usually shifts from what was found to what happened and what should happen next.

This is where our forensic and project advisory teams often work together. Our forensic specialists investigate the cause and origin of observed damage, evaluate liability where appropriate, and develop repair recommendations. Project advisory helps owners move from those technical findings into repair planning, construction management, documentation, scheduling, and completion. We do not serve as the design professional, but we frequently help owners oversee designers, contractors, and the repair process itself.

A technical repair plan typically addresses several key considerations, which may include:

What caused the condition?

How far does the issue extend?

What repair or monitoring options make sense?

What claims, insurance, or documentation issues need attention?

What record should be maintained through completion?

Keep in mind, owners still have to decide what gets repaired now, what can be monitored, what belongs in the capital plan, and what needs to be preserved for insurance, claims, or future due diligence.

Earlier Visibility Creates More Options

Hidden exterior risks become most expensive when owners discover them after decisions are already in motion. Once tenants are affected, financing is underway, an insurer is asking questions, or a transaction is on the line, the owner has less flexibility and less time.

Mr. Russell is the Senior Managing Director for Vertex in the Project Advisory Group. He has a Massachusetts Construction Supervisors License (unlimited). Mr. Russell is experienced in Design, Design Management, Construction Management, Owner's Project Management, Construction Defect Claim, Investigation, and Property, and Casualty Claim Investigation.

Gurtej Singh, Managing Director in Vertex’s Project Advisory Services, leads complex capital programs with a focus on risk reduction, schedule certainty, and value realization across diverse markets.